BLOG

Businesses have Options for Technology Leadership Positions

To say that technology continues to affect how businesses operate and interact with customers and prospects would be an understatement. According to the Business Software Market Size report issued by market researchers Mordor Intelligence, the global market size for commercial software is projected to reach $650 million this year and $1.10 trillion by 2029.

And that’s just software. Companies must also contend with technological issues such as hardware, skilled labor, strategy and cybersecurity. Just one of the resulting demands that this pressure is putting on businesses is a keen need for tech leadership.

If your company has grown to the point where it could use an executive-level employee with specialized knowledge of and laser focus on technology issues, you have plenty of options.

Positions to consider

Here are some of the most widely used position titles for technology executives:

Chief Information Officer (CIO). This person is typically responsible for managing a company’s internal IT infrastructure and operations. In fact, an easy way to remember the purpose of this position is to replace the word “Information” with “Internal.” A CIO’s job is to oversee the purchase, implementation and proper use of technological systems and products that will maximize the efficiency and productivity of the business.

Chief Technology Officer (CTO). In contrast to a CIO, a CTO focuses on external processes — specifically with customers and vendors. This person usually oversees the development and eventual production of technological products or services that will meet customer needs and increase revenue. The position demands the ability to live on the cutting edge by doing constant research into tech trends while also being highly collaborative with employees and vendors.

Chief Digital Officer (CDO). For some companies, the CIO and/or CTO are so busy with their respective job duties that they’re unable to look very far ahead. This is where a CDO typically comes into play. The primary purpose of this position is to spot new markets, channels or even business models that the company can target, explore and perhaps eventually profit from. So, while a CIO looks internally and a CTO looks externally, a CDO’s gaze is set on a more distant horizon.

Chief Artificial Intelligence Officer (CAIO). Did you really think you were going to make it through a technology article without reading about AI? Yes, more and more businesses are taking on executives whose primary responsibility is to create the company’s overall AI strategy and ensure it:

Aligns with the business’s overall strategic goals, and

Enhances the company’s digital transformation, which many businesses are continuing to undergo as they adapt to new technologies.

CAIOs are also typically responsible for understanding the global and national regulatory environments regarding AI, as well as ensuring the business uses AI ethically.

Big decision

Adding an executive-level position to your company is clearly a big decision. Along with making a sizable outlay for compensation and benefits, you’ll likely spend considerable time and resources on the search and onboarding processes. So be sure to discuss the matter thoroughly with your existing leadership team and professional advisors. FMD can help you identify and project all the costs involved.

5 Steps to Creating a Pay Transparency Strategy

Today’s job seekers and employees have grown accustomed to having an incredible amount of information at their fingertips. As a result, many businesses find that failing to adequately disclose certain things negatively impacts their relationships with these parties.

Take pay transparency, for example. This is the practice, or lack thereof, of a company openly sharing its compensation philosophy, policies and procedures with job candidates, employees and even the public. It typically means disclosing pay ranges or rates for specific positions, as well as clearly explaining how raises, bonuses and commissions are determined.

You’re not alone if your business has yet to formalize or articulate its pay transparency strategy. In its 2024 Global Pay Transparency Report, released in January of this year, global consultancy Mercer reported that only 19% of U.S. companies have a pay transparency strategy. Here are five general steps to creating one:

1. Conduct a payroll audit. Over time, your company may have developed a relatively complex compensation structure and payroll system. By meticulously evaluating and identifying all related expenditures under a formal audit, you can determine what information you need to share and which data points should remain confidential.

You may also catch inconsistencies and disparities that need to be addressed. Ultimately, an audit can provide the raw data you need to understand whether and how your company’s compensation aligns with the roles and responsibilities of each position.

2. Define or refine compensation criteria. To be transparent about pay, your business needs clear and consistent criteria for how it arrived — and will arrive — at compensation-related decisions. If such criteria are already in place, you may need to refine the language used to describe them. Again, your objective is to clearly explain to job candidates and employees how your company makes pay decisions so you can reduce or eliminate any perception of bias or unfairness.

3. Develop a communications “substrategy.” Under your broader pay transparency strategy, your company must have a comprehensive substrategy for communicating about compensation with job candidates, employees and, if you so choose, the public. There are many ways to go about this, and the details will depend on your company’s size, industry, mission and other factors. However, common aspects of a communications substrategy include:

Providing written guidelines explaining your compensation philosophy and structure,

Supplementing those guidelines with an internal FAQs document,

Holding companywide or department-specific Q&A sessions, and

Using digital platforms to share updates and issue reminders.

4. Train and rely on supervisors. Your people managers must be the frontline champions and communicators of your pay transparency strategy. Unfortunately, many companies struggle with this. In the aforementioned Mercer report, 37% of U.S. companies identified managers’ inability to explain compensation programs as their biggest challenge in this area.

Naturally, it all begins with training. Once you’ve defined or refined your compensation criteria and developed a communications substrategy, invest the time and resources into educating supervisors (and higher-level managers) about them. These individuals need to become experts who can discuss your business’s compensation philosophy, policies, procedures and decisions. And it’s critical that their messaging be accurate and consistent to prevent misunderstandings and misinformation.

5. Get input from professional advisors. Before you roll out a formal pay transparency strategy, ask for input from external parties. Doing so is especially important for small businesses that may have only a few voices involved in the planning process.

For example, a qualified employment attorney can help ensure your strategy is legally compliant and limit your potential exposure to lawsuits. And don’t forget FMD — we’d be happy to assist you in conducting a payroll audit, identifying all compensation-related expenses and aligning your strategy with your business objectives.

Are Your Employees Suffering from Retirement Plan Leakage?

Today’s small to midsize businesses are often urged to help employees improve their financial wellness. And for good reason: Financially struggling workers tend to have higher stress and anxiety levels. They may be less productive and more prone to errors. Some might even decide to commit fraud.

One hallmark of an employee facing serious financial trouble is “retirement plan leakage.” This term refers to the withdrawal of account funds before retirement age for reasons other than retirement. If your company sponsors a qualified plan, such as a 401(k), be sure you’re at least aware of this risk — and strongly consider taking steps to address it.

Potential dangers

Some business owners might say, “If my plan participants want to blow their retirement savings, that’s not my problem.” And there’s no denying that your employees are free to manage their finances any way they choose.

However, retirement plan leakage does raise potential dangers for your company. For starters, it may lead to higher plan expenses. Fees are often determined on a per-account or per-participant basis. When a plan loses funds to leakage, total assets and individual account sizes shrink, which hurts administrative efficiency and raises costs.

More broadly, as mentioned, employees taking pre-retirement withdrawals generally indicates they’re facing unusual financial challenges. This can lead to all the negative consequences we mentioned above — and others.

For example, workers who raid their accounts may be unable to retire when they reach retirement age. So, they might stick around longer but be less engaged, helpful and collaborative. Employees not near retirement age may take on second jobs or “side gigs” that distract them from their duties. And it’s unfortunately worth repeating: Motivation to commit fraud likely increases.

Mitigation measures

Perhaps the most important thing business owners can do to limit leakage is educate and remind employees about how pre-retirement withdrawals diminish their accounts and can delay their anticipated retirement dates. While you’re at it, provide broader financial education to help workers better manage living expenses, amass savings, and minimize or avoid the need for early withdrawals.

In addition, one recent and relevant development to keep in mind is the introduction of “pension-linked” emergency savings accounts (PLESAs) under the SECURE 2.0 law. Employers that sponsor certain defined contribution plans, including 401(k)s, can offer these accounts to employees who aren’t highly compensated per the IRS definition. Additional rules and limits apply, but PLESAs can serve as “firewalls” to protect participants from having to raid their retirement accounts when crises happen.

Some companies launch their own emergency loan programs, with funds repayable through payroll deductions. Others have revised their plan designs to reduce the number of situations in which participants can take out hardship withdrawals or loans.

Pernicious problem

It’s probably impossible to eliminate leakage from every one of your participants’ accounts. However, awareness — both on your part and those participants’ — is critical to limiting the damage that this pernicious problem can cause. FMD can help you identify and evaluate all the costs associated with your qualified retirement plan, as well as other fringe benefits you sponsor.

How businesses can better retain their salespeople

The U.S. job market has largely stabilized since the historic disruption of the pandemic and the unusual fluctuations that followed. But the fact remains that employee retention is mission-critical for businesses. Retaining employees is still generally less expensive than finding and hiring new ones. And strong retention is one of the hallmarks of a healthy employer brand.

One role that’s been historically challenging to retain is salesperson. In many industries, sales departments have higher turnover rates than other departments. If this has been the case at your company, don’t give up hope. There are ways to address the challenge.

Lay out the welcome mat

For starters, don’t focus retention efforts only on current salespeople. Begin during hiring and ramp up with onboarding. A rushed, confusing, or cold approach to hiring can get things off on the wrong foot. In such cases, new hires tend to enter the workplace cautiously or skeptically, with their eyes on the exit sign rather than the “upper floors” of a company.

Onboarding is also immensely important. Many salespeople tell horror stories of being shown to a cubicle with nothing but a telephone on the desk and told to “Get to it.” With so many people still working remotely, a new sales hire might not even get that much attention. Welcome new employees warmly, provide ample training, and perhaps give them a mentor to help them get comfortable with your business and its culture.

Incentivize your team

Even when hiring and onboarding go well, most employees will still consider a competitor’s job offer if the pay is right. So, to improve your chances of retaining top sales producers and their customers, consider financial incentives.

Offering retention bonuses and rewards for maintaining or increasing sales — in addition to existing compensation plans — can help. Make such incentives easy to understand and clearly achievable. Although interim bonus programs might be expensive in the near term, they can stabilize sales and prevent sharp declines.

When successful, a bonus program will help you generate more long-term revenue to offset the immediate costs. That said, financial incentives need to be carefully designed so they don’t adversely affect cash flow or leave your business vulnerable to fraud.

Give them a voice

Salespeople interact with customers and prospects in ways many other employees don’t. As a result, they may have some great ideas for capitalizing on your company’s strengths and shoring up its weaknesses.

Look into forming a sales leadership team to help evaluate the potential benefits and risks of goals proposed during strategic planning. The team should include two to four top sellers who are given some relief from their regular responsibilities so they can offer feedback and contribute ideas from their distinctive perspectives. The sales leadership team can also:

Serve as a clearinghouse for customer concerns and competitor strategies,

Collaborate with the marketing department to improve messaging about current or upcoming product or service offerings, and

Participate in developing new products or services based on customer feedback and demand.

Above all, giving your salespeople a voice in the strategic direction of the company can help them feel more invested in the success of the business and motivated to stay put.

Assume nothing

Business owners and their leadership teams should never assume they can’t solve the dilemma of high turnover in the sales department. The answer often lies in proactively investigating the problem and then taking appropriate steps to help salespeople feel more welcomed and appreciated. FMD can help your company calculate turnover rate, identify and track its hiring and employment costs, and assess the feasibility of financial incentives.

3 Areas of Focus for Companies Looking to Control Costs

Controlling costs is fundamental for every business. But where and how to address this challenge can change over time based on various economic and logistical factors.

Earlier this year, global consultancy Boston Consulting Group published a report entitled The CEO’s Guide to Costs and Growth. Within it were the results of a survey of 600 C-suite executives that found, among other things, cost management was a top priority for respondents heading into 2024. According to the survey, three of the top categories for cost-cutting initiatives were:

1. Supply chain / manufacturing. Not every company incurs manufacturing costs, but most have a supply chain. Costs and delays in this area soared during the pandemic because of global disruptions and backups. Since then, some sense of normalcy has returned, though that doesn’t mean managing supply chain costs has become easy.

Many companies find that most of their spending is done with just a few vendors. By identifying these vendors and consolidating spending with them, you may be able to put yourself in a stronger position to negotiate volume discounts. Consolidating your supplier base also tends to streamline the administrative work associated with purchasing.

It also pays to really know your suppliers. One way to gather an abundance of relevant information is to conduct a supplier audit. This is a formal process for collecting key data regarding each supplier’s performance to manage quality control and ensure you’re getting an acceptable return on investment.

2. Labor/nonlabor overhead. Controlling labor costs is tricky in today’s environment. Many industries are facing skilled labor shortages, meaning businesses would love to spend more on labor if they could find people to fill those positions. Nevertheless, with payroll being such a dominant expense category for most companies, it’s critical to monitor these costs and prevent overspending.

A logical first step in managing labor costs is to know how much you’re spending. And the answer isn’t as simple as looking at the total gross wages you pay out every month or year. You need to know the actual and total amount of these costs. Fortunately, there’s a metric for that. Labor burden rate reflects the additional costs that companies incur beyond gross wages. These generally include expenses such as payroll taxes, workers’ compensation insurance, and fringe benefits. Knowing your labor burden rate can enable you to truly “right-size” your workforce.

Beyond that, outsourcing remains an option for mitigating labor costs — especially given the vast pool of independent contractors now available. Although you’ll obviously incur costs when outsourcing, the time and labor cost that it saves you could end up a net gain. Carefully chosen and implemented technology upgrades can provide similar results.

3. Marketing/sales. Much like labor, strong marketing, and sales are critical to most businesses operating today. So, skimping on their related costs typically isn’t going to pay off. But, of course, you also need to ensure a strong return on investment.

Again, choosing and monitoring the right metrics can prove useful here. The optimal ones tend to vary by industry and company type, but some of the most widely used for marketing purposes include lead conversion rate, click-through rate for online ads, and cost per lead. Popular sales metrics include total revenue, year-over-year growth, and average customer lifetime value.

Whether it’s sales metrics, labor burden rate, or supply chain management, getting objective, professional advice can help you and your leadership team obtain an accurate picture of what’s going on with your costs and target feasible solutions. Please consider the FMD team for assistance.

Does Your Company Have an EAP? If so, be Mindful of Compliance

Many businesses have established employee assistance programs (EAPs) to help their workforces deal with the mental health, substance abuse, and financial challenges that have become so widely recognized in modern society.

EAPs are voluntary and confidential work-based intervention programs designed to help employees and their dependents deal with issues that may be affecting their mental health and job performance. These may include workplace stress, grief, depression, marriage/family problems, psychological disorders, financial troubles, and alcohol and drug dependency.

Whether your company is considering an EAP or already offers one, among the most important factors to keep in mind is compliance.

Start with ERISA

Several different federal laws may come into play with EAPs. A good place to start when studying your compliance risks is the Employee Retirement Income Security Act (ERISA). The law’s provisions address critical compliance matters such as creating a plan document and Summary Plan Description, performing fiduciary duties, following claims procedures, and filing IRS Form 5500, “Annual Return/Report of Employee Benefit Plan.”

Although most people associate ERISA with qualified health care and retirement plans, the law can be applicable to EAPs depending on how a particular program is structured and what benefits it provides. Generally, a fringe benefit is considered an ERISA welfare benefit plan if it’s a plan, fund, or program established or maintained by an employer to provide ERISA-listed benefits, which include medical services.

The category of ERISA-listed benefits most likely to be provided by an EAP is medical care or benefits. Mental health counseling — whether for substance abuse, stress, or other issues — is considered medical care. Accordingly, an EAP providing mental health counseling will probably be subject to ERISA. On the other hand, an EAP that provides only referrals and general information, and isn’t staffed by trained counselors, likely isn’t an ERISA plan.

Bear in mind that EAPs that primarily use referrals could still be considered to provide medical benefits if the individuals handling initial phone consultations and making the referrals are trained in an applicable field, such as psychology or social work. If an EAP provides any benefit subject to ERISA, then the entire program must comply with the law — even if it also provides non-ERISA benefits.

Check up on other laws

EAPs considered to be group health plans are also typically subject to the Consolidated Omnibus Budget Reconciliation Act (commonly known as “COBRA”) and certain other group health plan mandates, including mental health parity.

Also, keep in mind that EAPs that receive medical information from participants — even if the programs only make referrals and don’t provide medical care — must comply with privacy and security rules under the Health Insurance Portability and Accountability Act (HIPAA).

In addition, EAPs providing medical care or treatment could trigger certain provisions of the Affordable Care Act (ACA). EAPs meeting specified criteria, however, can be defined as an “excepted benefit” not subject to HIPAA portability or certain ACA requirements.

Cover all bases

Given the rising awareness and acceptance of mental health care alone, EAPs could become as common as health insurance and retirement plans in many companies’ employee benefit packages.

Whether you’re thinking about one or already have an EAP up and running, it’s a good idea to consult an attorney regarding your company’s compliance risks. Meanwhile, please FMD for help identifying and tracking the costs involved, as well as understanding the tax impact.

IRS Issues Final Regulations on Inherited IRAs

The IRS has published new regulations relevant to taxpayers subject to the “10-year rule” for required minimum distributions (RMDs) from inherited IRAs or other defined contribution plans. The final regs, which take this year, require many beneficiaries to take annual RMDs in the 10 years following the deceased’s death.

SECURE Act ended stretch IRAs

The genesis of the new regs dates back to the 2019 enactment of the Setting Every Community Up for Retirement Enhancement (SECURE) Act. One of the many changes in that tax law was the elimination of so-called “stretch IRAs.”

Previously, all beneficiaries of inherited IRAs could stretch RMDs over their entire life expectancies. Younger heirs in particular benefited by taking smaller distributions for decades, deferring taxes while the accounts grew. These heirs also could pass on the IRAs to later generations, deferring the taxes even longer.

The SECURE Act created limitations on which heirs can stretch IRAs. These limits are intended to force beneficiaries to take distributions and expedite the collection of taxes. Specifically, for IRA owners or defined contribution plan participants who died in 2020 or later, only “eligible designated beneficiaries” (EDB) are permitted to stretch out payments over their life expectancies. The following heirs are considered eligible for this favorable treatment:

Surviving spouses,

Children younger than “the age of majority,”

Individuals with disabilities,

Chronically ill individuals, and

Individuals who are no more than 10 years younger than the account owner.

All other heirs (known as designated beneficiaries) are required to take the entire balance of the account within 10 years of the death, regardless of whether the deceased died before, on, or after the required beginning date (RBD) of his or her RMDs.

Note: In 2023, under another law, the age at which account owners must begin taking RMDs increased from 72 to 73, pushing the RBD date to April 1 of the year after the account owner turns 73. The age is slated to jump to 75 in 2033.

Proposed regs muddied the waters

In February 2022, the IRS issued proposed regs addressing the 10-year rule — and they brought some bad news for many affected heirs. The proposed regs provided that, if the deceased dies on or after the RBD, designated beneficiaries must take their taxable RMDs in years one through nine after death (based on their life expectancies), receiving the balance in the tenth year. A lump-sum distribution at the end of 10 years wouldn’t be allowed.

The IRS soon heard from confused taxpayers who had recently inherited IRAs or defined contribution plans and didn’t know when they were required to start taking RMDs. Beneficiaries could have been hit with a penalty based on the amounts that should have been distributed but weren’t. This penalty was 50% before 2023 but was lowered to 25% starting in 2023 (or 10% if a corrective distribution was made in a timely manner). The plans themselves could have been disqualified for failing to make RMDs.

As a result, the IRS issued a series of waivers on enforcement of the 10-year rule. With the release of the final regulations, the waivers will come to an end after 2024.

Final regs settle the matter

The IRS reviewed comments on the proposed regs suggesting that if the deceased began taking RMDs before death, the designated beneficiaries shouldn’t be required to continue the annual distributions as long as the remaining account balance is fully distributed within 10 years of death. The final regs instead require these beneficiaries to continue receiving annual distributions.

If the deceased hadn’t begun taking his or her RMDs, though, the 10-year rule is somewhat different. While the account has to be fully liquidated under the same timeline, no annual distributions are required. That gives beneficiaries more opportunity for tax planning.

To illustrate, let’s say that a designated beneficiary inherited an IRA in 2021 from a family member who had begun to take RMDs. Under the waivers, the beneficiary needn’t take RMDs for 2022 through 2024. The beneficiary must, however, take annual RMDs for 2025 through 2030, with the account fully distributed by the end of 2031. Had the deceased not started taking RMDs however, the beneficiary would have the flexibility to not take any distributions in 2025 through 2030. So long as the account was fully liquidated by the end of 2031, the beneficiary would be in compliance.

Additional proposed regs

The IRS released another set of proposed regs regarding other RMD-related changes made by SECURE 2.0, including the age when individuals born in 1959 must begin taking RMDs. Under the proposed regs, the “applicable age” for them would be 73 years.

They also include rules addressing:

The purchase of an annuity with part of an employee’s defined contribution plan account,

Distributions from designated Roth accounts,

Corrective distributions,

Spousal elections after a participant’s death,

Divorce after the purchase of a qualifying longevity annuity contract, and

Outright distributions to a trust beneficiary.

The proposed regs take effect in 2025.

Timing matters

It’s important to realize that even though RMDs from an inherited IRA aren’t yet required, that doesn’t mean a beneficiary shouldn’t take distributions. If you’ve inherited an IRA or a defined contribution plan and are unsure of whether you should be taking RMDs, contact us. We’d be pleased to help you determine the best course of action for your tax situation.

3 Ways Businesses Can Get More Bang for Their Marketing Bucks

Most small to midsize businesses today operate in tough, competitive environments. That means it’s imperative to identify and reach the right customers and prospects.

However, unlike large companies, your business probably doesn’t have a massive marketing department with seemingly limitless resources. You’ve got to pursue savvy campaigns while also controlling costs. Here are three fundamental ways to get more bang for your marketing bucks.

1. Set a budget, rinse, repeat

Many companies, particularly start-ups and small businesses, engage in “marketing by desperation.” That is, they throw money at the problem haphazardly and hope for good results. A better strategy is to take a step back and set a realistic marketing budget based on factors such as:

Projected annual revenue (one rule of thumb is to allocate 5% to 10% of annual gross revenue to marketing, but this may not always be applicable),

Industry benchmarks (such as what similar-sized businesses in your industry spend on marketing), and

Growth goals (more aggressive growth may call for more dollars allocated).

Unfortunately, you can’t take a “set-it-and-forget-it” approach to your marketing budget. Every quarter, or at least at year end, compare your “marketing spend” to return on investment (ROI) using clear, verifiable financial metrics. Look for both 1) wasteful spending that you can eliminate or reallocate to other parts of the business, and 2) successful spending strategies that you can use for future campaigns. Regular budgetary reviews and adjustments will help your company adapt to industry and market changes without over- or underfunding marketing efforts.

2. Use metrics and technology to assess campaigns

One of the great things about marketing today is that many different metrics can help fine-tune your efforts. Examples include number of leads generated, lead conversion rate, and customer acquisition cost. An analytics-driven approach allows you to precisely measure the performance of your marketing campaigns.

Calculating these and other metrics shouldn’t involve pen and paper! You can use various technology tools to gather data, generate reports, and track progress. For example, if you use Google Business, it offers Google Analytics. This tool helps businesses track and analyze website traffic and visitor behavior. Other platforms, including most social media apps, offer similar functionality.

To take things to the next level, assuming you haven’t already, consider investing in customer relationship management software. Carefully selected and implemented, one of these solutions can allow you to input, gather, track, and analyze massive amounts of data to support marketing campaigns.

3. Avoid common mistakes

As you look to increase marketing ROI, watch out for common mistakes. First, don’t ignore the importance of meticulously defining your target audience. Although casting a wide net may seem like a good idea, doing so often leads to inconsistent results and wasted spending.

Second, don’t go overboard on paid ads. There are many forms of these online — including ads associated with search engines, websites, social media platforms, and video channels. On the plus side, they may yield quick results. However, they can also drain your marketing budget if you don’t manage them diligently. A best practice is to start with a small number of paid ads (even just one), test different ways to use them, and scale up based on positive results.

Last, never lose sight of the power of referrals. Word of mouth remains perhaps the most cost-effective way to market your business. Encourage satisfied customers to leave positive reviews on your website and social media channels. Consider offering discounts or freebies for referrals or online shout-outs.

Maximize positive impact

At the end of the day, getting a solid ROI from marketing is much more than simply cutting costs. You have to maximize the positive impact of your spending. Contact your FMD advisor for help creating and maintaining marketing budgets that align with your strategic goals and integrate well with your company’s other operational areas.

So Many KPIs, So Much Time: An Overview for Businesses

From the moment they launch their companies, business owners are urged to use key performance indicators (KPIs) to monitor performance. And for good reason: When you drive a car, you’ve got to keep an eye on the gauges to keep from going too fast and know when it’s time to service the vehicle. The same logic applies to running a business.

As you may have noticed, however, there are many KPIs to choose from. Perhaps you’ve tried tracking some for a while and others after that, only to become overwhelmed by too much information. Sometimes it helps to back up and review the general concept of KPIs so you can revisit which ones are likely best for your business.

Financial Metrics

One way to make choosing KPIs easier is to separate them into two broad categories: financial and nonfinancial. Starting with the former, you can subdivide financial metrics into smaller buckets based on strategic objectives. Examples include:

Growth. Like most business owners, you’re probably looking to grow your company over time. However, if not carefully planned for and tightly controlled, growth can land a company in hot water or even put it out of business. So, to manage growth, you may want to monitor basic KPIs such as:

Debt to equity: total debt / shareholders’ equity, and

Debt to tangible net worth: total debt / net worth – intangible assets.

Cash flow management. Maintaining or, better yet, strengthening cash flow is certainly a good aspiration for any company. Poor cash flow — not slow sales or lagging profits — often leads businesses into crises. To help keep the dollars moving, you may want to keep a close eye on:

Current ratio: current assets / current liabilities, and

Days sales outstanding: accounts receivable / credit sales × number of days.

Inventory optimization. If your company maintains inventory, you’ll no doubt want to set annual, semiannual or quarterly objectives for how to best move items on and off your shelves. Many businesses waste money by allowing slow-moving inventory to sit idle for too long. To optimize inventory management, consider KPIs such as:

Inventory turnover: cost of goods sold / average inventory, and

Average days to sell inventory: average inventory/cost of goods sold × number of days in period.

Nonfinancial Metrics

Not every KPI you track needs to relate to dollars and cents. Companies often use nonfinancial KPIs to set goals, track progress, and determine incentives in areas such as customer service, sales, marketing and production. Here are two examples:

Let’s say you decide to set a goal to resolve customer complaints faster. To determine where you stand, you could calculate average resolution time. This KPI is usually expressed as total time to resolve all complaints divided by number of complaints resolved. In many industries, a common benchmark is 24 to 48 hours.

Perhaps you want to increase the number of sales leads you close. In this case, the KPI could be sales close rate, which is typically calculated by dividing number of closed deals by number of sales leads. Benchmarks for this metric vary by industry, but somewhere around 20% is generally considered good.

Nonfinancial KPIs enable you to do more than just say, “Let’s provide better customer service!” or “Let’s close more sales!” They allow you to assign specific data points to business activities, so you can objectively determine whether you’re getting better at them.

Scalable measurements

The sheer number of KPIs — both financial and nonfinancial — will probably only grow. The good news is, you’ve got time. Choose a handful that make the most sense for your company and track them over a substantial period. Then, make adjustments based on the level of insight they provide.

You can also scale up how many metrics you track as your business grows or scale them down if you’re pumping the brakes. FMD can help you identify the optimal KPIs for your company right now and integrate new ones in the months or years ahead.

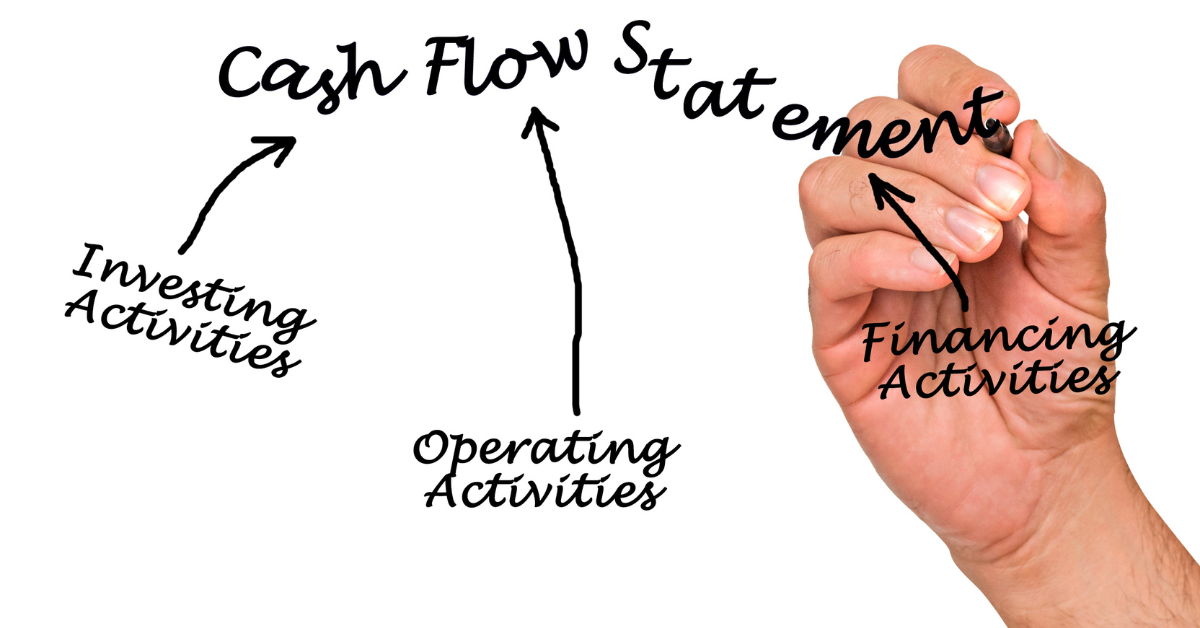

Business owners: Be sure you’re properly classifying cash flows

Properly prepared financial statements provide a wealth of information about your company. But the operative words there are “properly prepared.” Classifying information accurately isn’t always easy — especially as the business grows and its financial transactions become more complex.

Case in point: your statement of cash flows. Customarily, it shows the sources (money entering) and uses (money exiting) of cash. That may sound simple enough, but optimally classifying different cash flows can be complicated.

Under U.S. Generally Accepted Accounting Principles (GAAP), statements of cash flows are typically organized into three sections: 1) cash flows from operating activities, 2) cash flows from investing activities, and 3) cash flows from financing activities. Let’s take a closer look at each.

Operating activities

This section of the statement of cash flows usually starts with accrual-basis net income. Then, it’s adjusted for items related to normal business operations. Examples include income taxes; stock-based compensation; gains or losses on asset sales; and net changes in accounts receivable, inventory, prepaid assets, accrued expenses and payables.

The cash flows from operating activities section is also adjusted for depreciation and amortization. These noncash expenses reflect wear and tear on equipment and other fixed assets.

The bottom of the section shows the cash used in producing and delivering goods or providing services. Several successive years of negative operating cash flows can signal that a business is struggling and may be headed toward liquidation or a forced sale.

Investing activities

If your company buys or sells property, equipment or marketable securities, such transactions should show up in the cash flows from investing activities section. It reveals whether a business is reinvesting in its future operations — or divesting assets for emergency funds.

Business acquisitions and disposals are generally reported in this section, too. However, contingent payments from an acquisition are classified as cash flows from investing activities only if they’re paid soon after the acquisition date. Later contingent payments are classified as financing outflows. Any payment over the liability is classified as an operations outflow.

Financing activities

This third section of the statement of cash flows shows your company’s ability to obtain funds from either debt from lenders or equity from investors. It includes new loan proceeds, principal repayments, dividends paid, issuances of securities or bonds, additional capital contributions by owners, and stock repurchases.

Noncash transactions are reported in a separate schedule at the bottom of the statement of cash flows or in a narrative footnote disclosure. For example, suppose a business buys equipment using loan proceeds. In such a case, the transaction would typically appear at the bottom of the statement rather than as a cash outflow from investing activities and an inflow from financing activities.

Other examples of noncash financing transactions are:

Issuing stock to pay off long-term debt, and

Converting preferred stock to common stock.

In those two instances and others, no cash changes hands. Nonetheless, financial statement users, such as investors and lenders, want to know about and understand these transactions.

Help is available

As you can see, deciding how to classify some transactions to comply with GAAP can be tricky. Whenever confusion or uncertainty arises, give us a call. We can work with you and your accounting team to make the best decision. We can also help you improve your financial reporting in other ways.

© 2024

Marketing your B2B company via the right channels

For business-to-business (B2B) companies, effective marketing begins with credible and attention-grabbing messaging. But you’ve also got to choose the right channels. Believe it or not, some “old school” approaches remain viable. And of course, your B2B digital marketing game must be strong.

Press releases

It doesn’t get much more old school than this. Launching a new product? Introducing a new service? Opening a new location? When your company has big news, getting the word out with a press release can still pay off.

Be sure to follow best practices when writing them. Include the topic’s who, what, where, when and why. Add a quote of at least two sentences from you (the business owner) or another leadership team member. If appropriate and feasible, also incorporate customer or industry expert testimonials.

In addition, maintain an updated contact list of press release recipients. Customarily, these include media outlets, business news aggregators, key customers, prospects, investors and other stakeholders.

Authoritative articles

Do you know of one or more industry publications that would be a good fit for sharing your knowledge and experience? If so, and you’re comfortable with the written word, submit an idea for an article.

Getting published in the right places can position you (or a suitable staff member) as a technical expert in your field. For example, write an article explaining why the types of products or services that your company provides are more important than ever in your industry. Or write one on the technologies that are most affecting your industry and what you expect the future to look like.

But be careful: Publications generally won’t accept content that comes off as advertising. Write articles as objectively as possible with only subtle mentions of your company’s offerings.

There are other options, too. You could pen an opinion piece on how a legislative proposal will likely affect your industry. Or you might write a tips-oriented article that lends itself to an online publication looking for short, easy-to-read content. For any type of article, insist on attribution for you and your business.

Digital marketing

Over the last couple of decades, digital marketing has taken the business world by storm. This holds true for B2B companies as well. Virtual channels are many, with possibilities including your website, blogs, various social media platforms and podcasts.

In fact, there are so many digital avenues you could travel down, you may find the concept overwhelming. There’s also a high risk of burnout. Many businesses add blogs to their websites or open social media accounts, post a few things, and then disappear into the ether. That’s not a good look for companies trying to establish themselves as industry experts.

To be successful at digital marketing, or even just to keep your website up to date, create an editorial calendar and stick to it. Devise a strategy to push out quality content regularly on your optimal channels. It can be authored by you, one or more qualified staff members, or a content marketing provider.

Critical role

Companies that provide B2B products or services must establish credibility and demonstrate expertise in whatever industry they operate. Marketing plays a critical role in this effort, so choose your channels carefully. We can help you identify, quantify and analyze all your marketing costs.

© 2024

Surprise IT failures pose a major financial risk to companies

It’s every business owner’s nightmare. You wake up in the morning, or perhaps in the middle of the night, and see that dreaded message: “We’re down.” It could be your website, e-commerce platform or some other mission-critical information technology (IT) system. All you know is it’s down and your company is losing money by the hour.

A report released this past June by cybersecurity solutions provider Splunk drove home the financial risk of unanticipated downtime for today’s businesses. Entitled The Hidden Costs of Downtime, it was produced in partnership with Oxford Economics researchers who surveyed 2,000 large-company executives worldwide. They found that the total cost of downtime for responding businesses, including direct and hidden costs, was a staggering $400 billion annually. The biggest direct cost was revenue loss, averaging $49 million annually per company.

More than revenue

Of course, such losses for large businesses will be proportionately higher given the bigger amounts of revenue they generate. However, small to midsize companies are arguably at even greater risk because they may not be able to readily absorb any substantial revenue losses.

Diminished revenue is just one of the direct costs of surprise IT failures. Others include regulatory fines, blown IT budgets from coping with crises and elevated insurance premiums. Hidden costs may arise from diminished shareholder value (for publicly traded businesses), reduced productivity and brand/reputational damage.

Common threats

Worried yet? The good news is that your business can proactively address the threat of unanticipated technological downtime. The first step is to conduct a formal risk assessment to identify the most likely causes of IT failures based on the distinctive features of your systems and users.

Spoiler alert: You’ll probably find cyberattacks, such as phishing and ransomware scams, are your biggest threat. Unfortunately, these crimes have become so common that you should probably operate under the assumption that you’ll incur attacks fairly often, be they minor or major.

Indeed, the Splunk report attributed 56% of downtime incidents to cybersecurity breaches. Not far behind, however, were software or IT infrastructure failures. These caused 44% of reported downtime. And whether it was a cyberattack or a technological gaffe, human error was identified as the chief underlying cause. So, don’t be surprised if a risk assessment also identifies your employees as a major threat to your company’s ability to stay up and running.

Key strategies

Once you’ve pinpointed the IT risks with the greatest probability of occurring, you can address them. Just a few key strategies to strongly consider include:

Tracking incidents carefully. When downtime occurs, you should have an incident response plan in place to investigate and resolve the matter — as well as to record all pertinent details. Look for trends: As incidents happen more often, the likelihood of a major crisis increases.

Investing wisely in cybersecurity. Today’s companies need to look at substantial investment in cybersecurity as a cost of doing business. However, you must still scale these expenditures to your actual needs and risk level.

Training new hires and regularly upskilling employees. The Splunk report highlighted an essential truth: No matter how technologically advanced businesses become, people still make the difference.

Establishing a disaster recovery plan. As the saying goes, expect the best but plan for the worst. Implement a comprehensive plan involving sound backup policies and procedures, as well as recovery time and point objectives.

Assessing and testing regularly. The risk assessment mentioned above shouldn’t be a one-time thing. Adhere to a strict schedule of assessments and “stress tests” of mission-critical systems.

Continuous improvement

To prevent surprise IT failures at your company, apply a mindset of continuous improvement to all aspects of your policies, procedures and infrastructure. Our firm can help you identify and manage your technology costs.

© 2024

Turnaround acquisitions are risky growth opportunities for today’s companies

When it comes to growth, businesses have two broad options. First, there’s organic growth — that is, progress made through internal efforts such as boosting sales, expanding into other markets, innovating new products or services, and improving operational efficiency. Second, there’s inorganic growth, which is achieved through externally focused activities such as mergers and acquisitions (M&A), and strategic partnerships.

Organic growth is, without a doubt, imperative to the success of most companies. But occasionally, or more often if you pursue M&A proactively, you may encounter the opportunity to acquire a troubled business. Although “turnaround acquisitions” can yield considerable long-term rewards, acquiring a struggling concern poses greater risks than buying a financially sound company.

Due diligence

Generally, successful turnaround acquisitions begin by identifying a floundering business with hidden value, such as untapped market potential, poor (but replaceable) leadership or excessive (yet fixable) costs.

But be careful: You’ve got to fully understand the target company’s core business — specifically, its profit drivers and roadblocks — before you start drawing up a deal. If you rush into the acquisition or let emotions cloud your judgment, you could misjudge its financial condition and, ultimately, devise an ineffective course of rehabilitative action. This is why so many successful turnarounds are conducted by buyers in the same industry as the sellers or by investors, such as private equity firms, that specialize in particular types of companies.

During the due diligence phase, pinpoint the source(s) of your target’s distress. Common examples include excessive fixed costs, lack of skilled labor, decreased demand for its products or services, and overwhelming debt. Then, determine what, if any, corrective measures can be taken.

Don’t be surprised to find hidden liabilities, such as pending legal actions or outstanding tax liabilities. Then again, you also might find potential sources of value, such as unclaimed tax breaks or undervalued proprietary technologies.

Cash management

Another critical step in due diligence is identifying cash flows, both in and out. Determine what products or services drive revenue and which costs hinder profitability. Would it make sense to divest the business of unprofitable products or services, subsidiaries, divisions, or real estate?

Implementing a long-term cash-management plan based on reasonable forecasts is also critical. Revenue-generating and cost-cutting measures — such as eliminating excessive overtime pay, lowering utility bills, and collecting unbilled or overdue accounts receivable — can often be achieved following a thorough evaluation of accounting controls and procedures.

Reliable due diligence hinges on whether the target company’s accounting and financial reporting systems can produce the appropriate data. If these systems don’t accurately capture transactions and fully list assets and liabilities, you’ll likely encounter some unpleasant surprises and struggle to turn around the business.

Buyers vs. sellers

Parties to a business acquisition generally structure the deal as a sale of either assets or stock. Buyers usually prefer asset deals, which allow them to select the most desirable items from a target company’s balance sheet. In addition, buyers typically receive a step-up in basis on the acquired assets, which lowers future tax obligations. And they’re often able to negotiate new contracts, licenses, titles and permits.

On the other hand, sellers generally prefer to sell stock, not assets. Selling stock simplifies the deal, and tax obligations are usually lower for sellers. However, a stock sale may be riskier for the buyer because the struggling target business remains operational while the buyer takes on its debts and legal obligations. Buyers also inherit sellers’ existing depreciation schedules and tax basis in target companies’ assets.

Reasonable assurance

For any prospective turnaround acquisition, you’ve got to establish reasonable assurance that the return on investment will likely exceed the acquisition’s immediate costs and ongoing risks. We can help you gather and analyze the financial reporting and tax-related information associated with any prospective M&A transaction.

© 2024

How businesses can better retain their sales people

The U.S. job market has largely stabilized since the historic disruption of the pandemic and the unusual fluctuations that followed. But the fact remains that employee retention is mission-critical for businesses. Retaining employees is still generally less expensive than finding and hiring new ones. And strong retention is one of the hallmarks of a healthy employer brand.

One role that’s been historically challenging to retain is salesperson. In many industries, sales departments have higher turnover rates than other departments. If this has been the case at your company, don’t give up hope. There are ways to address the challenge.

Lay out the welcome mat

For starters, don’t focus retention efforts only on current salespeople. Begin during hiring and ramp up with onboarding. A rushed, confusing or cold approach to hiring can get things off on the wrong foot. In such cases, new hires tend to enter the workplace cautiously or skeptically, with their eyes on the exit sign rather than the “upper floors” of a company.

Onboarding is also immensely important. Many salespeople tell horror stories of being shown to a cubicle with nothing but a telephone on the desk and told to “Get to it.” With so many people still working remotely, a new sales hire might not even get that much attention. Welcome new employees warmly, provide ample training, and perhaps give them a mentor to help them get comfortable with your business and its culture.

Incentivize your team

Even when hiring and onboarding go well, most employees will still consider a competitor’s job offer if the pay is right. So, to improve your chances of retaining top sales producers and their customers, consider financial incentives.

Offering retention bonuses and rewards for maintaining or increasing sales — in addition to existing compensation plans — can help. Make such incentives easy to understand and clearly achievable. Although interim bonus programs might be expensive in the near term, they can stabilize sales and prevent sharp declines.

When successful, a bonus program will help you generate more long-term revenue to offset the immediate costs. That said, financial incentives need to be carefully designed so they don’t adversely affect cash flow or leave your business vulnerable to fraud.

Give them a voice

Salespeople interact with customers and prospects in ways many other employees don’t. As a result, they may have some great ideas for capitalizing on your company’s strengths and shoring up its weaknesses.

Look into forming a sales leadership team to help evaluate the potential benefits and risks of goals proposed during strategic planning. The team should include two to four top sellers who are given some relief from their regular responsibilities so they can offer feedback and contribute ideas from their distinctive perspectives. The sales leadership team can also:

Serve as a clearinghouse for customer concerns and competitor strategies,

Collaborate with the marketing department to improve messaging about current or upcoming product or service offerings, and

Participate in developing new products or services based on customer feedback and demand.

Above all, giving your salespeople a voice in the strategic direction of the company can help them feel more invested in the success of the business and motivated to stay put.

Assume nothing

Business owners and their leadership teams should never assume they can’t solve the dilemma of high turnover in the sales department. The answer often lies in proactively investigating the problem and then taking appropriate steps to help salespeople feel more welcomed and appreciated. We can help your company calculate turnover rate, identify and track its hiring and employment costs, and assess the feasibility of financial incentives.

© 2024

Working capital management is critical to business success

Success in business is often measured in profitability — and that’s hard to argue with. However, liquidity is critical to reaching the point where a company can consistently turn a profit.

Even if you pile up sales to the sky, your bottom line won’t flourish unless you have the cash to fund operations to fulfill all those orders. The good news is there’s a tried-and-true way to stay liquid while you grow your company. It’s called working capital management.

Multifunctional metric

Working capital is a metric — current assets minus current liabilities — that’s traditionally used to measure liquidity. Essentially, it’s the amount of accessible cash you need to support short-term business operations. Regularly calculating working capital can help you and your leadership team answer questions such as:

Do we have enough current assets to cover current obligations?

How fast could we convert those assets to cash if we needed to?

What short-term assets are available for loan collateral?

Another way to evaluate liquidity is the working capital ratio: current assets divided by current liabilities. A healthy working capital ratio varies from industry to industry, but it’s generally considered to be 1.5 to 2. A ratio below 1.0 typically signals impending liquidity problems.

For yet another perspective on working capital, compare it to total assets and annual revenue. From this angle, working capital becomes a measure of efficiency.

Working capital requirement

The amount of working capital your company needs, known as its working capital requirement, depends on the costs of your sales cycle, operational expenses and current debt payments.

Fundamentally, you need enough working capital to finance the gap between payments from customers and payments to suppliers, vendors, lenders and others. To optimize your business’s working capital requirement, focus primarily on three key areas: 1) accounts receivable, 2) accounts payable and 3) inventory.

High liquidity generally equates with low credit risk. But having too much cash tied up in working capital may detract from important growth initiatives such as:

Expanding into new markets,

Buying better equipment or technology,

Launching new products or services, and

Paying down debt.

Failure to pursue capital investment opportunities can also compromise business value over the long run.

3 critical areas

The right approach to working capital management will obviously vary from company to company depending on factors such as size, industry, mission and market. However, as mentioned, there are three primary areas of the business to focus on:

1. Accounts receivable. The faster your company collects from customers, the more readily it can manage debt and capitalize on opportunities. Possible solutions include tighter credit policies, early bird discounts and collections-based sales compensation. Also, continuously improve your administrative processes to eliminate inefficiencies.

2. Accounts payable. From a working capital perspective, you generally want to delay paying bills as long as possible — particularly those from noncritical suppliers, vendors or other parties. One exception to this is when you can qualify for early bird discounts. Naturally, delaying payments should never drift into late payments or nonpayment, which can damage your business credit rating.

3. Inventory. If your company maintains inventory, recognize the challenge it presents to working capital management. Excessive inventory levels may dangerously reduce liquidity because of restocking, storage, obsolescence, insurance and security costs. Then again, insufficient inventory levels can frustrate customers and hurt sales. Be sure to give your inventory the “TLC” it deserves — including regular technology upgrades and strategic reconsideration of optimal levels.

The right balance

It isn’t easy to strike the right balance of maintaining enough liquidity to operate smoothly while also saving funds for capital investments and an emergency cash reserve. Our firm can help you assess precisely where your working capital stands and identify ways to manage it better.

© 2024

IT strategy showdown: Enterprise architecture vs. Agile

Few, if any, companies can operate successfully today without the right information technology (IT) strategy. And as businesses grow, their IT needs and infrastructures become even more complex and costly.

This push and pull of managing growth while grappling with tech has brought two broad approaches to IT strategy to the forefront: enterprise architecture and Agile. Let’s look at both so you can contemplate where your company stands and whether an adjustment may be warranted.

Following a blueprint

As its name implies, enterprise architecture is a strategic philosophy that focuses on mindfully designing or adapting a companywide framework for choosing, implementing, operating and supporting technology.

Think of an architect drawing up a blueprint for a commercial building — every aspect of that structure will be thought through ahead of time to suit the size, operational needs and mission of the company. So it goes with enterprise architecture, which seeks to ensure every IT decision and move:

Aligns with the goals of the business. Everything done technologically flows from the company’s current goals as established through ongoing strategic planning. So, for example, no new software acquisitions or upgrades can occur without approval from the enterprise architecture unit, which can be a dedicated department or a special committee.

Complies with standardization and organization protocols. Businesses using enterprise architecture construct their IT systems to integrate seamlessly and follow stated rules for access, use, upgrades, cybersecurity and so forth. They also organize their systems to support digital transformation (digitalizing all areas of the business) and adapt relatively quickly to technological changes.

In some cases, complies with an established framework. There are various widely accepted enterprise architecture frameworks for companies that don’t wish to do it all themselves or would like a starting point. These include The Open Group Architecture Framework, the Zachman Framework and ArchiMate.

Being project-focused

Rather than being a top-down blueprint for IT strategy, Agile generally approaches business tech on a project-by-project basis. The idea is to be as nimble as possible. Some of its key features include:

Breaking up IT projects into small pieces (often called “sprints” or “iterations”),

Collaborating closely with customers (whether internal or external),

Using cross-functional teams, rather than only IT staff,

Focusing on continuous improvement during and after projects,

Emphasizing flexibility over strict protocols, and

Valuing interpersonal collaboration over processes and tools.

Like enterprise architecture, Agile also has different time-tested versions that many types of organizations have used. These include Scrum and Kanban.

Leaning one way or the other

Not too long ago, many large companies began leaning away from enterprise architecture and toward Agile. Some experts attribute this to increased reliance on cloud-based storage and software, which tends to decentralize IT infrastructure.

Earlier this year, however, market research firm Forrester released the results of a survey of 559 technology professionals worldwide in its Modern Technology Operations Survey, 2023 report. Of respondents who work for large enterprises, 55% said their organizations had an enterprise architecture unit. That’s an 8% increase from the 47% reported in the 2022 version.

Some experts believe the renewed emphasis on enterprise architecture could be a reaction to a couple potential downsides of relying largely or solely on Agile. That is, businesses running small, speedy IT projects with little to no oversight may encounter higher “technical debt” — the predicament of getting suboptimal project results that lead to costly downtime and rework. Companies may also suffer from “vendor sprawl,” a term that describes having too many software providers because Agile project teams act independently.

Managing the costs

To be clear, enterprise architecture and Agile aren’t mutually exclusive. Many companies use both approaches to some extent. Work with your leadership team and professional advisors to devise and execute your best IT strategy. We can help you quantify, track and manage your company’s technology costs.

© 2024

Businesses must stay on guard against invoice fraud

Fraud is a pernicious problem for companies of all shapes and sizes. One broad type of crime that seems to be thriving as of late is invoice fraud.

In the second quarter of 2024, accounts payable software provider Medius released the results of a survey of 1,533 senior finance executives in the United States and United Kingdom. Respondents reported that their teams had seen, on average, 13 cases of attempted invoice fraud and nine cases of successful invoice fraud in the preceding 12 months. The average per-incident loss in the United States was $133,000 — which adds up to about $1.2 million annually.

Typical schemes

Invoice fraud can be perpetrated in various ways. Among the most common varieties is fraudulent billing. In billing schemes, a real or fake vendor sends an invoice for goods or services that the business never received — and may not have ordered in the first place.

Overbilling schemes are similar. Your company may have received goods it ordered, but the vendor’s invoice is higher than agreed upon. Duplicate billing, on the other hand, is where a fraud perpetrator sends you the same invoice more than once, even though you’ve already paid.

Employees sometimes commit invoice fraud as well. This can happen when a manager approves payments for personal purchases. In other cases, a manager might create fictitious vendors, issue invoices from the fake vendors and approve the invoices for payment.

Such schemes generally are more successful when employees collude. For example, one perpetrator might work in receiving and the other in accounts payable. Or a receiving worker might collude with a vendor or other outside party.

Best practices

The good news is there are some best practices that businesses can follow to discourage would-be perpetrators and catch those who try to commit invoice fraud. These include:

Know with whom you’re doing business. Verify the identity of any new supplier or vendor before working with that entity. Research its ownership, operating history, registered address and customer reviews. Also, ask for references so you can contact other companies that can vouch for its legitimacy.

Follow a thorough approval process. Establish a firm “no rubber stamp” policy for invoices. Train accounts payable staff to review them for red flags, such as unexpected changes in the amounts due or unusual payment terms. Manual alterations to an invoice should require additional scrutiny, as should the first several invoices from new vendors.

Instruct employees to contact an issuing vendor if anything seems strange or inaccurate about its invoice. In cases where the response lacks credibility or raises additional concerns, your business should decline to pay until the matter is resolved.

Implement additional antifraud controls as well. For instance, before approving payment, accounts payable staff should confirm with your receiving department that goods were delivered and check invoices against previous ones from the same vendor to ensure there are no discrepancies. Also, you may want to require more than one person to approve certain invoices for payment — such as those at or above a specified amount.

Leverage technology. Automating your accounts payable process can help prevent and detect invoice fraud. And, as you might expect, artificial intelligence (AI) is having an impact here.

One AI-driven technology called optical character recognition (OCR) can scan and read invoices to verify that line items and charged amounts match those vendors quoted you per your company’s financial records. OCR minimizes employee intervention, hinders collusion and makes diverting payments to personal accounts harder.

Decisive action

As the aforementioned survey indicates, invoice fraud is likely widespread. Be sure to put policies and procedures in place to prevent it as well as to respond swiftly and decisively if you suspect wrongdoing. Our firm can help you assess your accounts payable processes for efficiency, completeness and security.

© 2024

Which leadership skills are essential to strategic planning?

To help ensure continued stability and profitability, businesses need to engage in some form of strategic planning. A recent survey by insurance giant Travelers drives home this point.

In its 2024 CFO Study: A Travelers Special Report, the insurer surveyed 610 chief financial officers (CFOs) from companies with 500 or more employees in various industries. One of the questions posed was: What are the most valuable skills needed by today’s CFOs?

One might assume their answers would relate to being able to crunch numbers or understand complex regulations. But the top skill, coming from 62% of respondents, was “Strategic planning for future company success and resiliency.”

5 critical skills

Along with being somewhat surprising, the survey result begs the question: Which leadership skills, specifically, are essential to strategic planning? Among the five most important are the ability to:

1. View the company realistically and aspirationally. Strategic planning starts with a grounded view of where the company currently stands and a shared vision for where it should go. You and your leadership team need accurate information — including properly prepared financial statements, tax returns and sales reports — to establish a common perception of the state of the business. And from there, you need to be able to reach a mutually agreed-upon vision for the future.

2. Analyze the industry and market — and foresee impending changes. Everyone should be up to speed on the state of your industry and market from the pertinent perspective. Your CFO, for example, needs to be able to report on key performance indicators that place your company’s financial status in the context of industry averages and explain how those metrics compare to competitors in your market.

What’s more, everyone needs to develop the ability to make reasonable, fact-based predictions on where the industry and market are headed. Not every prediction will come true, but you’ve got to be able to forecast effectively as a team.

3. Understand customers and anticipate their needs. Again, from every member’s distinctive perspective, your leadership team needs to know who your customers truly are. This is where your marketing executive can come into play, laying out all the key features and demographics of those who buy your products or services.

Then you’ve got to put in the teamwork to determine what your customers want now and, even more important, what they will want in the future. That latter point is perhaps the biggest challenge of strategic planning.

4. Recognize the capabilities and resources of the business. Your company can operate only within realistic limits. These include the size of its workforce, the skill level of employees, and the availability of resources such as liquidity, physical assets and up-to-date technology.

Every member of your leadership team needs to be on the same page about what your business can realistically do before you decide where you can realistically go. Having a balanced collective of voices — financial, operational and technological — is critical.

5. Communicate effectively. Many companies struggle with strategic planning, not because of a shortage of ideas, but because of a failure to communicate. Leaders who tend to “silo” themselves and the knowledge of their respective departments can be particularly inhibitive. There are also those whose behavior or communication style is simply counterproductive. Continually work on improving how you and your leadership team communicate.

Confident growth

So, does your leadership team have all the requisite skills to succeed at strategic planning? If not, there are certainly ways to upskill your key players through training and performance management. We can help your business gather the financial information it needs to plan for the future confidently and decisively.

© 2024

Brand audits can help companies in a variety of ways

A strong brand can help boost revenue, while a weaker one may reduce sales opportunities and stifle growth.

Like many business owners, you’ve probably spent considerable time and energy crafting your company’s brand. Doing so has likely involved coming up with a memorable business name and logo, communicating with customers in a distinctive manner, and, above all, building a strong reputation in your market.

So, how’s all that going? Although your bottom line can certainly tell you a thing or two about the current success of your business, brand strength can be a little trickier to put a finger on. That’s why many companies conduct brand audits — essentially, formal reviews of a brand’s efficacy and market standing.

Data to gather

There are many ways to conduct a brand audit. The optimal steps for your business will depend on factors such as your industry, your company size and the popularity of your brand.

But most audits have certain things in common. For starters, they generally rely on information you already have on hand or could easily generate. Examples include:

Sales data. One objective of a brand audit is to identify sales-related key performance indicators and trends that may relate to branding. Essentially, if sales have slumped, is your brand partly to blame? And if so, why?

Website analytics. Brand audits usually investigate whether site traffic is trending upward or downward. They also typically determine how much time visitors spend on your site and on which pages. A strong brand will draw consistent visitors who tend to stick around. A weaker one is often indicated by a large number of accidental visitors who leave quickly.

Social media interactions. Although social media has its challenges and downsides, one enormous benefit is that each of your accounts should provide a wealth of interaction data. Brand audits can analyze this information over time to assess brand strength — and determine whether it’s rising or falling.

Customers and employees

Most brand audits also involve gathering the thoughts and opinions of two major constituencies: customers and employees.

Customers, of course, represent the richest source of insight into brand strength. Brand audits can involve surveys that posit various questions to customers and prospects about your brand. But such a survey needs to be carefully designed. You’ve got to keep it short, clear and easy to complete. Most are now conducted online.

Employees can also tell you things about your brand that you might not know or haven’t thought about. Your sales staff, for instance, could be getting feedback — positive or negative — from customers and prospects. So, an employee survey focused on brand-related issues can be a useful part of an audit.

More than marketing

Generally, brand audits are conducted for marketing purposes. They can help your marketing department determine how to enhance your brand — or potentially even whether you need to undertake a full-blown rebrand. But regular brand audits can also benefit strategic planning. You may even discover that someone has been using your brand fraudulently!

Precisely who should conduct a brand audit typically depends on business size. Larger companies with sizable internal marketing teams may be able to do it themselves. But many small to midsize businesses turn to marketing consultants or agencies to do the job. Our firm can help you assess the costs of a brand audit, as well as gather and analyze some of the financial data involved.

© 2024

Business owners sometimes need to switch successors

For many business owners, choosing a successor is the most difficult task related to succession planning. Owners of family-owned businesses, who may have multiple children or other relatives to consider, particularly tend to struggle with this tough choice.

What’s worse, many business owners’ initial picks for a successor don’t work out. Over time, the chosen person can prove to be unqualified, incapable or unwilling to fulfill a leadership role. If you find yourself in this situation, don’t panic. There are some measured steps you can take to resolve the matter.

Ask around

Before you dismiss your chosen successor, discuss the situation with several objective parties. These might include professional advisors, such as your CPA and attorney, as well as trusted family members, friends or colleagues with business experience.

Your goal is to determine whether your perception is off the mark. You may think, for instance, that your successor lacks the necessary skills to run your company. But the person might simply have a different leadership style than you do. Talking with others may help you put things in perspective.

Look for ways to help

If you come to believe that, with some work, your successor may still be capable of running the business after all, meet with the person. State your concerns and outline what must change.

And don’t forget to listen. Ask why your successor is having the difficulties you’ve pointed out. Perhaps it’s a lack of formal training in one aspect of the job. In such cases, there may be a class that can help provide the needed education, or maybe more mentoring from you might solve the problem.